As Canada phases out coal at home, it continues exporting it overseas, pushing planet-warming greenhouse gas emissions even higher and making tons of money in the process. In this series, Canada’s National Observer digs into efforts to end coal, barriers in the way and solutions needed to get off fossil fuels for good.

Canada’s largest banks are betting heavily on metallurgical coal. Collectively, Scotiabank, RBC, TD, BMO and CIBC have loaned or invested more than US$20 billion to companies mining it. This represents a staggering financial risk as efforts to slash global greenhouse gas emissions push the steelmaking industry to replace coal with greener alternatives.

The towering sum of money, calculated by research outfit Reclaim Finance, is used to increase metallurgical coal production around the world, and in Canada, to fuel a growing demand for steel. Unlike thermal coal burned to generate power, metallurgical coal is used to make coke, which is fed into blast furnaces at steel plants. Demand for steel is projected to grow more than a third by 2050, according to the International Energy Agency (IEA), a world-leading authority on energy supply and demand. One way to meet the need is to build new coal mines and expand existing ones.

However, the IEA projects demand for metallurgical coal will drop to a third of current levels by 2050 because solutions to emission-intensive steel are quickly emerging. Electric furnaces, recycling used steel and green hydrogen can all be used to decarbonize the sector, which is why the IEA is clear: no new metallurgical coal mines are required to meet demand.

Even as forecasts cast doubt on the future of coal, more than 100 companies are planning 138 metallurgical coal projects around the world. Of those, 60 per cent are new mines and 40 per cent are mine expansions, according to the Global Energy Monitor. Together, they would add 406 million tonnes of coal each year to global stockpiles.

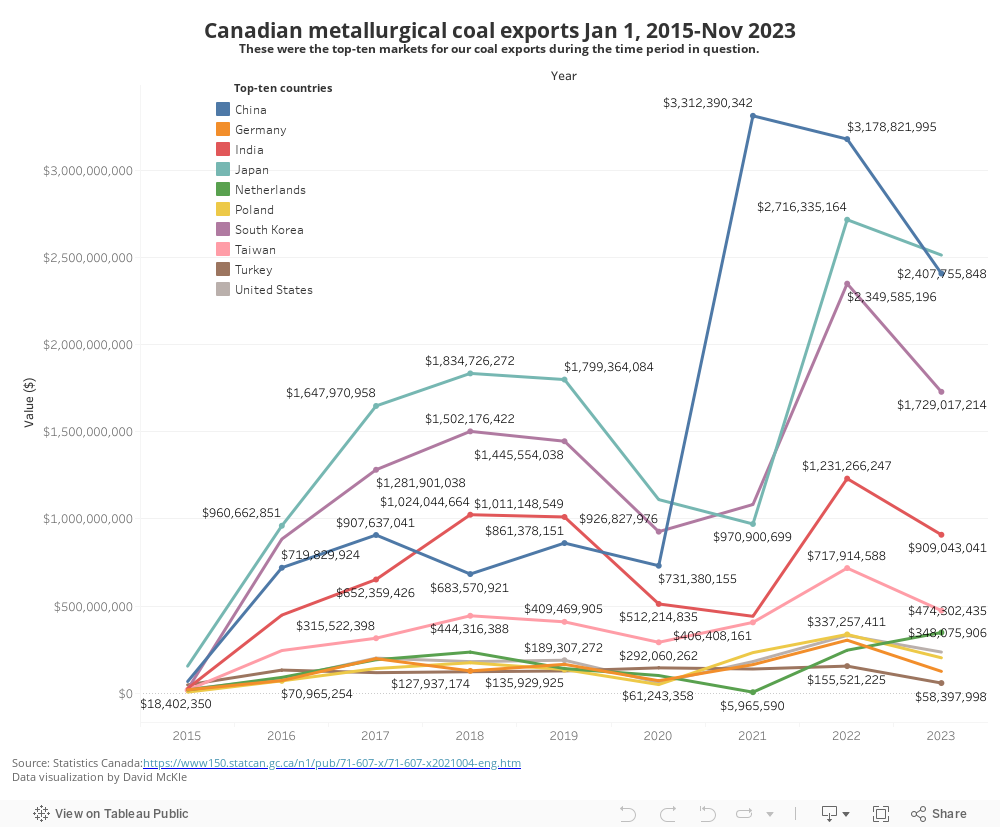

With demand projected to fall and supply set to grow, Canada’s National Observer wanted to understand the risks and challenges for the metallurgical coal industry in Canada and its financial backers. A data analysis tracking coal exports from 2015 to November 2023 found over $58 billion worth of metallurgical coal was exported, representing an important part of the economy at risk from the energy transition if not effectively managed. Canada’s National Observer also found policies to limit financial risks are virtually non-existent.

Thermal coal mines have long been well-recognized as at risk from the energy transition as countries phase out coal-fired power plants, meaning they are likely to become money-losing stranded assets. Metallurgical coal mines have not faced the same scrutiny because it was long believed demand for metallurgical coal would rise with demand for steel. Because global population growth and increased urbanization, which drive steel demand, are not expected to slow any time soon, proponents of metallurgical coal felt they were on a sure footing.

But, according to researchers with Reclaim Finance, metallurgical coal mines are also at significant risk of losing value as steel companies decarbonize.

"The solutions to decarbonize steel exist, and the transition to new technologies is underway. And yet, financial players continue to add fuel to the climate fire, by financially supporting the development of new mines,” said Reclaim Finance industry campaigner Cynthia Rocamora, in a statement. “This is a threat to the economy as these new mines risk becoming stranded assets, and it is a disaster for the climate.

“The world needs to realize that literally all coal policies existing today are missing a big chunk of coal — metallurgical coal,” she added. “This goes for financial institutions, but also for government policies, as the proposed ban on private finance for coal being championed by France and the U.S. at COP28 [showed].”

In recent years, technological advancements have laid bare a new reality: Fossil-free, decarbonized steel is possible and scalable — it just needs investment. A study published in June by Agora Industry said it is technically feasible to have a net-zero iron and steel sector by the early 2040s, without relying on carbon credits or carbon capture technologies.

In other words, steelmaking can quickly go green if it can get the cash needed to pull off the transition. And if that happens, as required to avoid disastrous climate change, demand for metallurgical coal will plummet.

Dirty steel

Like thermal coal used for generating electricity, metallurgical coal is highly polluting and must be phased out to limit global warming. The steel sector is responsible for an estimated 11 per cent of global greenhouse gas emissions and without changing course, the sector is expected to burn 25 per cent of the world’s remaining carbon budget by 2050. That’s one reason why governments in Canada are subsidizing investments needed by steelmakers to decarbonize.

In Hamilton, ArcelorMittal confirmed in 2022 that it was moving ahead with an electric furnace at its Dofasco plant after securing $400 million from the federal government and $500 million from the Ontario government. Similarly, Algoma Steel in Sault Ste. Marie, Ont., received $420 million from Ottawa to help it transition to greener steel.

At the same time progress is being made, Canadian financial institutions are shovelling money into coal, making the problem worse. Ten per cent of global banking support for metallurgical coal companies comes from Canadian banks, Reclaim Finance found.

Research from Reclaim Finance notes Swiss commodity trading giant Glencore and Vancouver-headquartered Teck Resources are among the top clients for Canadian financial institutions, having received billions from RBC, Scotiabank, BMO, TD, CIBC, Sun Life and the Power Corporation of Canada. Collectively, those companies have provided over $20 billion worth of financing to metallurgical coal companies.

RBC declined to comment. Scotiabank, BMO, TD, CIBC, Sun Life and the Power Corporation did not return requests for comment.

Glencore-Teck deal reveals emerging corporate strategy

Climate-related risks to this profitable sector are a serious issue in the boardrooms of mining companies, although companies are making different bets based on what their investors want.

A blockbuster deal negotiated last year revealed the tectonic shift underway. Glencore, alongside two Asian steelmakers (Japan’s Nippon Steel and South Korea’s POSCO), agreed in mid-November to buy Teck’s coal business, called Elk Valley Resources, in a deal valued at US$8.9 billion. Teck CEO Jonathan Price explained the decision to sell was motivated by investor pressure.

“Shareholders have told us very clearly that they would like to see a separation of steelmaking coal from base metals,” Price told the Globe and Mail, explaining that investors are concerned about the environmental impacts of coal.

The Glencore-Teck deal illustrates the different decisions investors are making to manage the risks of the energy transition, Adam Scott, executive director of Shift: Action for Planet Wealth and Planet Health, a climate finance advocacy group, told Canada’s National Observer.

“Teck has clearly realized this asset will lose value [and] their met coal mining operations are actually something investors have told them: ‘We don't want to hold,’” he said. Appeasing investors who want to ditch dirty investments is why the metallurgical coal assets are being carved off into a separate entity as Teck pivots into critical minerals.

Meanwhile, “Glencore is going to try to get as much money out of the coal business as humanly possible, knowing full well that that's a declining market, and declining asset, over a longer period,” Scott explained.

“I think we're going to see a lot more examples where companies take legacy, high-liability, high-risk assets like that and put them in a separate entity so that investors can say: ‘OK, we'll put that in the risky part of my portfolio, but I don't want it over here in the ‘buy and hold’ category,’” he added.

If a company held onto its coal mines while trying to scale up clean alternatives, it’s signalling to investors that the risk of its mines becoming stranded is real and could threaten the company as a whole, Scott said.

“It makes much more sense to have two companies because investors want the renewable energy investment,” he said. “They do not want the legacy, declining, bottom-of-the-barrel junk asset.”

“Those are different asset classes … and the types of investors who want them are different.”

Practically, that means Canadian financial institutions are at a fork in the road reminiscent of oilsands production. For years now, as foreign banks try to clean up their portfolios, they have been pulling out of the oilsands due to the unacceptable greenhouse gas emissions, leaving Canadian banks to invest even further in the industry.

Now, foreign banks are starting to set policies to cut their direct investments in metallurgical coal. HSBC, Société Générale, BNP Paribas and CaixaBank have all set policies to rule out financing for new metallurgical coal mines and expansions — although HSBC has since helped finance Glencore to the tune of $1 billion through a general corporate financing bond. There is nothing stopping Glencore from using this money to finance its metallurgical coal expansion plans.

RBC, Scotiabank, BMO, TD, CIBC, Sun Life and the Power Corporation have not set any policies to limit their investments in metallurgical coal and did not return requests for comment about why that is.

“The world must urgently move away from coal-based steel production and financial institutions bear a crucial responsibility in accommodating this transition,” said Rocamora. “It’s time to stop all types of finance for all types of new coal projects — thermal and metallurgical included.”

— With files from David McKie

Comments

These are all good, safe bets. Not because green steel isn't possible, or that it won't work in practice; it may even be almost as cheap. It will just take a long time to take over the world. The world produces a staggering billion tonnes of steel per year: for some reason, I admit I'm unclear upon, we need 125kg of steel every year for every living human. (All those empty towers built by Evergrande in China, full of rebar; about 60kg per residence built).

We recycle quite a lot of steel, could do more, and will do more when "green steel" makes new steel more expensive - which will be another hammer-and-tongs fight to push out "black steel". But, we still need that billion tonnes a year, and you don't replace an industry of that size overnight because a few pilot plants worked out OK.

David Roberts, at "Volts" has just done a pod on the other big energy material, cement; they have high hopes for affordable cement from electrochemistry, but they aren't to their "kilotonne" plant yet, the serious pilot that will do 1000 tonnes per year of cement. Then they can tackle the first "megatonne" plant that makes a commercial amount, works towards commercial prices. By 2030, they may be building a hundred new "megatonne" plants, and the amount of "black cement" will start to ramp down, replaced with "green cement". But, that's ANOTHER billion-tonne-a-year industry, and there's just no way to build whole new cement and steel plants fast enough to replace them all by 2040. Well, 2040 would be a stretch-goal, possible with a global-sized Manhattan Project urgency.

It's an exciting 20 years coming, of rapid progress and industrial shift. But I just can't imagine a real world where it takes less than 20 years. Steel plants and cement plants are just very, very large expensive things with a million human-hours of labour, among other resources, embedded in each. There are no "steel plant factories" that punch out steel plants like cars.

So the coal market is ongoing, and necessary to all that steel - every wind turbine has many tonnes of steel in the monopole; more so out to sea.

Exemplary commentary. Kudos!

While it's true that purchase price has a lot of power and persuasion either way low or high, long term planning and life cycle accounting offer profound benefits for society.

Ripping and shipping raw metallurgical coal to China and importing cheap Chinese steel is commonly short term, highly myopic economic thinking. Bottom line stuff.

Making green steel at home with higher purchase prices (at least initially) also brings in new high paying jobs with built in multipliers spread through the domestic economy, expands the benefits of using local sources and suppliers with their own additional multipliers, and mitigates environmental impacts (even eliminates key pollutants).

All of these are financially measurable and counter the notion that cheaper is better.

One day sooner than we think, given its tremendous rate of conversion to renewables, China will be making green steel for export and will likely charge a premium for it. Canada will then need to pay more up front for steel while seeing its lucrative coal exports decrease with no clean industrial initiatives waiting in the wings at home with new jobs and fresh income tax revenue.

Bottom line thinking from corporate finance departments seeking bargains at the exclusion of long term planning will get us there very efficiently. This is one of the big reasons public policy needs to make it possible to assume a leadership role to ensure things like home made green steel will be a net benefit to society in spite of higher prices.

Wind turbine companies today are sensitive to the criticism about embedded carbon and waste. Recycling every part of a post-use turbine is now reaching common practice status. Land-based turbines are looking at certified plantation grown wood and waste wood fo

To make mass timber mast towers using tensioned steel rods inside for added strength.

Concrete and steel are still necessary for the foundations, but it's entirely possible to build and replace several towers bolted down to the same foundation several times for decades.

Sea-based wind turbines are now being floated in deep water on big pontoons, making them towable into port for rebuilding every decade or so. The generators are also being made orders of magnitude more powerful, therein minimizing the number of turbines and lowering the overall per megawatt cost, embedded carbon and material content.

It may take longer than we'd like to displace two billion tonnes of black steel and concrete worldwide, but it's interesting to realize that the price of green steel and cement will decrease as more is produced, and making them in Canada will pay for the differential over and over forever with jobs and spin offs if they are made at home.