On the fourth day of COP26, Mark Carney unveiled the army of financial giants he has recruited in the fight against climate change. More than 450 financial firms from across the world, including Canada’s Big Five banks, have joined Carney’s Glasgow Financial Alliance for Net Zero, a club that requires its members to follow certain sustainability standards.

That represents a total of US$130 trillion in assets nominally committed to reaching net-zero emissions by 2050.

“Make no mistake,” Carney, the former head of the Bank of Canada and the Bank of England, told the crowd at COP26. “The money is now there if the world truly wants to address climate change.”

While the country’s second-biggest pension fund, Caisse de dépôt et placement du Québec (CDPQ), joined the Glasgow alliance, the rest of the so-called Big Eight were noticeably absent as of the publishing of this article.

Critics have argued the Glasgow alliance is more “smoke and mirrors” than real climate action, especially because it does not include an explicit commitment to divest from fossil fuels. In fact, members of the alliance are still actively financing fossil fuel firms.

Complaints about smoke and mirrors notwithstanding, alliance membership is a beginning and represents a high-profile commitment to battling the climate crisis.

So, the absence of Canada's largest pension funds from the alliance, however symbolic, raises questions about that commitment.

The so-called Big Eight are the country’s largest and richest pension funds. What they do and how they invest matters — to the pensioners who depend on a steady retirement income, and to the Canadian economy, which needs the billions of dollars in investments to grow.

For their part, sustainable finance advocates interviewed by Canada's National Observer worry the Canadian pension funds’ widespread absence from Carney's alliance means they are not fully committed to the path to net-zero emissions.

“The fact that the Canadian Pension Plan [CPP], for example, couldn’t even bring itself to sign onto a very modest transition pledge — in terms of the demands it places on signatories — is noteworthy,” says James Rowe, an associate professor of environmental studies at the University of Victoria who has studied pension funds’ fossil fuel holdings.

So who are the Big Eight?

In descending order, they are the following:

- Canada Pension Plan Investment Board (CPPIB),

- Caisse de dépôt et placement du Québec (CDPQ),

- Ontario Teachers’ Pension Plan (OTPP),

- British Columbia Investment Management Corporation (BCI),

- Public Sector Pension Investment Board (PSPIB),

- Alberta Investment Management Corporation (AIMCo),

- OMERS (Ontario Municipal Employees Retirement System),

- Healthcare of Ontario Pension Plan (HOOPP).

Reuters reports five of the Big Eight increased their investments in the country’s top four oilsands producers by 147 per cent between 2020 and 2021.

Despite its relatively small population, Canada is home to two of the world’s 15 largest pension funds, CPP and CDPQ, which manage roughly $900 billion. The remaining six manage another $950 billion.

“[They have] a huge amount of market power,” says Rowe, adding their investing decisions can have outsized impacts on Canadian and global markets. As such, the speed at which they embrace a transition to a green economy “makes a difference.”

Over the last several years, Canada’s major pension funds have paid more attention to sustainability in several ways, including developing climate action plans, appointing chief risk officers, issuing responsible investment reports, and increasing their investments in renewables. In November 2020, the Big Eight CEOs issued a formal statement calling for companies and investors to provide complete and consistent ESG (environmental, social, and governance) disclosures.

But Rowe argues they are still moving far too slowly.

None of the funds responded to interview requests from Canada’s National Observer.

What stands in the way of decarbonization?

A central reason for the slow pace of change is inherent to the structure of pension funds themselves, says Scott Janzwood, deputy director of research and operations at the Cascade Institute, a sustainability advocacy organization in Victoria, B.C.

“Pensions are supposed to have super long-term time horizons, but that’s practically very difficult to incentivize,” he says.

Investors and fund managers receive bonuses based on the returns they earn within one or two years, not how their investments fare over decades. “Obviously, that incentivizes alpha-chasing and trying to outperform direct competitors in the very short term,” says Janzwood.

“They’re making all these short-term decisions, such as dumping money into building pipelines. Ultimately, those are harming the ability to have returns in the long run.”

Jessica Dempsey, an assistant professor at the University of Victoria who has analyzed pension funds’ fossil fuel holdings, says merely disclosing climate risk is not enough to change the behaviour of pension funds and the companies in which they invest. Even the Glasgow alliance, she adds, largely continues to emphasize voluntary decarbonization and disclosures “as though information about risks is enough to shift capital at the pace and scale we need.”

Dempsey says a lack of government action also contributes to the slow speed of pension funds’ decarbonization. “Too often, voluntary action gets in the way of the needed regulatory action,” says Dempsey.

Dempsey — along with other climate activists and progressive politicians — will pressure the federal Liberals to honour their platform promise to “require climate-related financial disclosures and the development of net-zero plans for federally regulated institutions, such as … pension funds …”

Pressure will also be on provincially regulated pension funds to follow suit.

Canadian pension funds falling behind global leaders

Canadian pension funds’ continued investments in oil, gas, and coal put them at odds with a global trend that has seen such institutions shun fossil fuels with increasing zeal.

In April, New York’s state pension divested from six Canadian oil companies. And in late October, the world’s largest pension fund, the Netherlands’ ABP, announced it would cease fossil fuel investments immediately and divest its US$17.4 billion of existing assets by 2023.

Canadian pension funds — and, in turn, everyday Canadians — could suffer if they fail to implement similar measures, critics argue. “We face a dichotomous choice here,” says Truzaar Dordi, a divestment activist, researcher and doctoral candidate at the University of Waterloo.

“If we continue to support the expansion of fossil fuel emissions, we will face a climate crisis. Alternatively, if we meet our climate targets, pension funds will face immense asset stranding” — for example, the devaluation of drilling equipment and oil left in the ground without a buyer.

“That will ultimately affect us as employees and retirees.”

What follows is a snapshot of the Big Eight in descending order of size.

The lowdown on the Big Eight

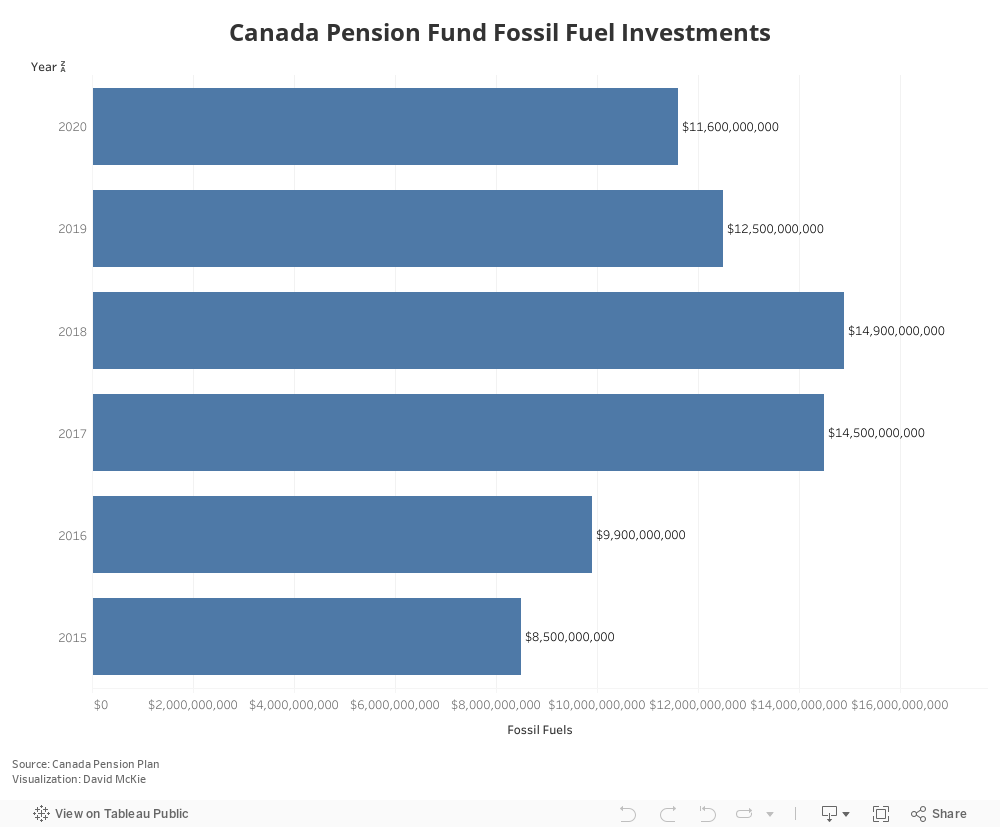

The Canada Pension Plan is Canada’s largest public pension plan whose assets have steadily grown. According to its annual report, the fund had $497.2 billion in net assets at the end of its March 2021 fiscal year, representing a 20.4 per cent return and a net income of $83.8 billion.

Although the fund lauds its investment in renewables, it still invests in fossil fuels, albeit in amounts equalling a small part of the plan’s total portfolio.

The pension plan did not respond to Canada’s National Observer’s request for an interview about its divestment plans. Instead, spokesman Frank Switzer steered us to its 2020 Sustainable Investing Report, and noted in his emailed response that “we expect our latest Sustainability Report to be published in coming weeks, which may be of interest.”

However, the plan has pushed back, reminding critics that its oil and gas investments made up a paltry 2.8 per cent of its net investments at the end of its March 2021 fiscal year, compared to 3.2 per cent in 2015. The plan also points to its investments in renewables, which climbed significantly during the same time period to $6.6 billion.

Canada’s second-largest pension fund

CDPQ is Quebec’s institutional investor, managing several public-sector pension plans and insurance programs.

As of June 30, six million Quebecers contributed to the fund.

Source: CDPQ

According to its June 30 “snapshot,” the fund had $390 billion in net assets, a 44 per cent increase from 2016. In addition to joining the Glasgow alliance, the fund also made news recently by announcing that it was pulling its investments out of the oilsands by 2022. However, it also announced continued support for companies abroad to “reduce the carbon intensity of their activities at the source.”

Advocates see the continued support as a contradiction, arguing CDPQ can’t pull out of the oilsands while continuing to invest in similar companies beyond Canada’s borders.

It is this kind of perceived mixed messaging about the need to help some companies decarbonize that continues to frustrate divestment advocates.

The CDPQ did not respond to Canada’s National Observer’s request for an interview.

Divesting and staying the course

With $227.7 billion in net assets (as of June 30) the Ontario Teachers’ Pension Plan is the country’s third-largest pension fund, holding diverse assets worldwide on behalf of Ontario’s 331,000 active and retired teachers.

Despite its commitment to achieve net-zero greenhouse gas emissions by 2050, the Ontario Teachers’ Pension Plan has been the subject of intense lobbying by activists pushing for total divestment. This, despite its recent announcement to beef up that commitment by aiming for “2025 and 2030 interim targets” to “dramatically” reduce emissions by 2050.

“Because of its size and influence,” concludes a so-called “toolkit” prepared by pension watchdog Shift Action, “the [plan’s] investment decisions play a major role in how quickly the world can transition to a zero-carbon economy while continuing to grow teachers’ pension savings in a warming world.”

Critics such as Rowe take issue with the decarbonization strategies of major institutions, which largely say they prefer to help fossil fuel companies transition to cleaner forms of energy extraction and production rather than divest outright.

Critics argue this constitutes a puzzling double standard. Pension funds are promising to decarbonize their portfolios, yet are still investing in fossil fuel companies that say they will transition to cleaner measures such as carbon capture and storage, which has received federal support.

The Ontario Teachers’ Pension Plan did not respond to an interview request, but in a recent question-and-answer document argues “engaged ownership” gives it a “seat at the table … to push for positive changes.”

Federal public servants’ ties to fossil fuels

The Public Sector Pension Investment Board (PSP) is the country’s fourth-largest pension fund, a Crown corporation that manages $204.5 billion on behalf of more than 900,000 active and retired federal public servants and members of the Canadian Armed Forces, RCMP, and Reserve Force.

According to its 2021 annual report, PSP has $12.6 billion in green assets. Alongside teachers’ and Ontario’s public sector pension plan, PSP also contributed to the US$7-billion Brookfield Global Transition Fund, a group dedicated to pivoting away from fossil fuels.

But, in the past two years, the pension fund has purchased massive stakes in AltaGas Canada, a company proposing fossil gas expansion in several provinces and states, and EG Group, one of the world’s largest gas station owners. German NGO Urgewald also reports that PSP has US$154 million worth of shares in the global coal industry.

Source: PSP

PSP declined an interview request. In an emailed response, a spokesperson said the pension fund plans to ramp up ESG disclosures and “views responsible investment as one of the most critical social, environmental and economic opportunities of our time. As a long-term investor, we proactively address ESG risks and opportunities as an integral part of our investment strategy.”

Fossil fuel entanglement on the West Coast

Canada’s fifth-biggest pension fund, the British Columbia Investment Management Corporation (BCI), manages $200 billion on behalf of 690,000 public servants, teachers, and others in B.C., plus insurance and benefit funds for a total of 2.5 million workers.

BCI’s investments in sustainable bonds. Source: BCI

Earlier this year, BCI pledged to invest $5 billion in sustainable bonds and reduce the carbon exposure in its global public equities portfolio by 30 per cent by 2025. It is also part of Climate Action 100+, a group that asks its members to reduce greenhouse gas emissions and reach net-zero emissions by 2050.

BCI refused Canada’s National Observer’s interview request. In a statement, spokesperson Ben O’Hara-Byrne wrote that “capitalizing on opportunities for value creation from the transition to a lower-carbon economy while mitigating systemic risks presented by climate change is core to BCI’s responsibility.

“We believe divestment is not an effective strategy for addressing long-term and persistent risks to our clients’ portfolios,” O’Hara-Byrne continued, in an argument similar to the one made by the Ontario teachers’ fund.

“Ownership gives BCI the right to raise concerns and influence a company on matters relating to ESG practices.”

According to BCI’s latest ESG report, it invests in more than two dozen fossil fuel-based energy companies, including Kinder Morgan, Imperial Oil, and ExxonMobil.

An overexposure to oil and gas in Alberta

With $123.4 billion in assets, the Alberta Investment Management Corporation (AIMCo) is Canada’s sixth-biggest pension fund, responsible for more than 30 pension, endowment, and government funds.

Though AIMCo has made sustainable strides in recent years — such as integrating ESG into investment decisions, investing $3.7 billion in no- or low-carbon infrastructure and renewables, and signing onto Climate Action 100+ — the pension fund’s own chief investment officer concedes it is overexposed to Alberta’s oil and gas industry.

According to AIMCo’s 2020 annual report, more than a quarter of the fund's $9.6-billion infrastructure investments are in pipelines and energy transportation and storage. This includes majority ownership stakes in the Coastal GasLink and the Northern Courier pipelines, among dozens of other fossil fuel investments.

A breakdown of AIMCo’s $9.6 billion in infrastructure assets. Source: AIMCo

AIMCo declined an interview request, instead directing Canada’s National Observer to the pension fund’s responsible investing policies, which promote a “voice over exit” philosophy of helping companies transition to lower carbon footprints.

The efficacy of that approach will be tested by AIMCo’s latest investment. In early November, it was part of a Brookfield-led consortium that offered US$7.7 billion to take over AusNet. The consortium says it plans to spend just as much integrating renewables into the electricity and fossil gas utility’s toolbox.

Assessing climate risk for Ontario’s municipal employees

The Ontario Municipal Employees Retirement System (OMERS) is the country’s seventh-largest pension plan. Representing more than 525,000 retired and working employees, the fund manages $105 billion.

“Investment decisions of funds like OMERS influence whether companies build electric cars and solar panels, or diesel engines and oil and gas infrastructure,” notes Shift Action’s analysis of the plan.

The plan says it has invested about $3.3 billion in clean energy, which represents about three per cent of its total portfolio.

The analysis also points out that OMERS has announced few targets, which means the plan's beneficiaries have “justified concerns that their pension fund invests in climate failure.”

OMERS declined an interview request, instead directing us to its latest sustainable investing report.

Ontario’s health system and its connection to fossil fuels

The Healthcare of Ontario Pension Plan (HOOPP) is the smallest of the Big Eight, managing $104 billion on behalf of roughly 400,000 of the province’s health-care workers.

As was the case with the previous funds, HOOPP declined an interview request.

In a written statement, Sarah Takaki, senior director of sustainable investing, said, “HOOPP members count on us to deliver on the pension promise, and to do so in a sustainable fashion. We take those joint responsibilities seriously, as outlined in our sustainable investing program.”

The program’s measures include integrating ESG into investment strategies, greening its real estate portfolio, reporting in line with the Task Force on Climate-related Financial Disclosures, and calling on the companies in which they invest to do the same.

By the end of 2020, HOOPP had invested $174 million in a portfolio of renewables in the U.S., with plans to invest $57 million more in 2021.

Source: HOOPP

“Despite its modest investments in climate solutions and green real estate and claims to take the climate crisis seriously,” a Shift Action report says, “HOOPP continues to invest hundreds of millions of dollars in the fossil fuel infrastructure and companies fuelling the climate crisis.”

A 2020 Corporate Knights analysis showed HOOPP has $762 million invested in companies involved in fossil fuels, deforestation, and anti-climate action lobbying.

The uncertain road ahead

During the days and months following COP26, pension funds, in addition to other large institutions such as banks, will be under increased pressure to divest with greater speed and explain what they are doing and why.

To date, explanations have been in short supply, as the pension funds refused several interview requests from Canada’s National Observer, opting instead to issue canned, generic statements that avoid tough questions about their fossil fuel investments.

However, based on explanations from their financial statements, it’s clear balancing the need to maximize returns on investments while decarbonizing their portfolios is challenging. The recent rebound of energy stocks makes the balancing act even trickier.

What’s also clear from the financial statements is the funds’ desire to have a “seat at the table,” arguing this gives them the necessary clout to push companies to transition to cleaner and greener energy.

Advocates are reading those same financial statements. But, so far, they’re not buying the argument.

Comments

Maybe it's not so much weighing carbon reduction against return to investors (though I'm not sure where else they'd expect to get a 20%+ annual return on investments) ... as a silly ruse around the meaning of "sustainability" and "carbon reductions."

First notice that almost all their "reduction" of their carbon portfolio is no reduction at all: just almost the same investment being based on an investment base 20% larger.

Then look at how close in their apologistics are words beginning "sustainab-" followed by examples of increasing or failure to decrease investments in carbon support, then "balanced" with a (usually smaller) bit of actually sustainable investing.

IOW, they seem to think they can increase "carbonizing" with one hand, and "trade" their good works against them. At that rate, they should perhaps just declare themselves carbon neutral now, and ??? say they'll sustain the balance in their portfolios right up to 2050.

It's one thing to invest to the benefit of their ultimate beneficiaries, another to shorten their lives. I guess from the POV of maximizing profits/performance/bonuses, it's probably a win/win/win. Except we all lose.

The thing I find completely galling is that the money going into those pension and insurance funds ultimately comes from taxpayers: we all pay, regardless of who the actual beneficiaries are. And we all lose when we don't deal as quickly as possible with climate change.